SMM May 28 News:

As of May 28, the most-traded SHFE zinc contract closed at 22,210 yuan/mt, down 230 yuan/mt (1.02%) for the month. In May, zinc prices remained in the doldrums, hitting a low of 22,070 yuan/mt at the beginning of the month before rebounding to a high of 22,915 yuan/mt mid-month. Overall, the price center declined noticeably compared to April. Entering June, as smelting capacity gradually ramps up, how will zinc prices perform?

Macro perspective. In early May, China and the U.S. resumed negotiations, easing trade tensions. Although China introduced a series of RRR cuts and interest rate cuts, these measures largely fell in line with expectations. Mid-month, the outcome of the Sino-U.S. talks was announced, with tariffs significantly reduced, improving macro sentiment and driving zinc prices higher. However, as market sentiment gradually digested the news, macro influence waned, and zinc prices resumed a fluctuating trend. Entering June, with the tariff issue resolved, the market awaits further macro guidance.

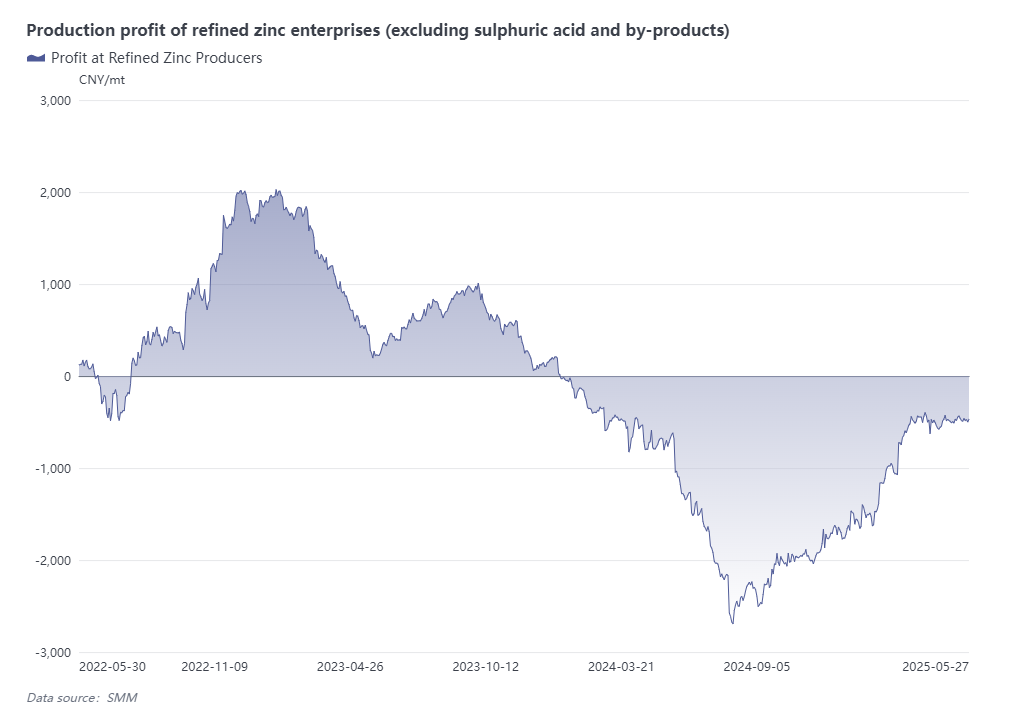

Supply side. Despite routine maintenance at some smelters in May, driven by sulphuric acid profits, production at certain smelters increased. Coupled with a large influx of imported zinc ingots into the domestic market, overall zinc ingot supply remained high in May. In June, zinc concentrate TCs continue to rise, boosting smelter production enthusiasm. Newly commissioned smelters in Henan and Yunnan have begun output, while production at previously idled smelters continues to recover. Overall, zinc ingot supply is expected to remain robust in June.

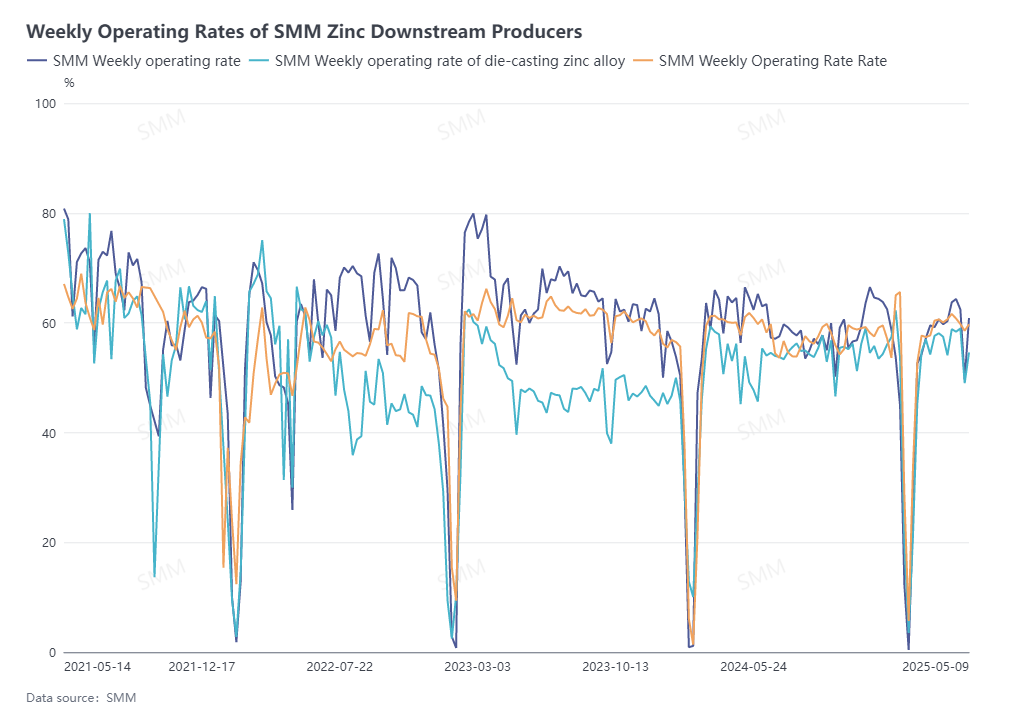

Demand side. With the easing of Sino-U.S. tariff tensions, downstream enterprises resumed production of previously suspended export orders mid-month. Overall orders and consumption remained firm, but with limited new export orders and a decline in domestic trade orders, downstream zinc demand showed no MoM growth in May. Entering June, as temperatures rise and the rainy season approaches, end-user sector orders may weaken further, while existing export orders continue to be digested. Zinc demand is expected to gradually soften in June.

Looking ahead to June, the fundamentals point to a supply-demand imbalance, with stronger supply and weaker demand. As zinc ingot production increases, social inventory may begin to accumulate, potentially weakening price support. Zinc prices could face downward pressure, warranting close attention to subsequent macro guidance and downstream consumption performance.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)